Earnings results often indicate what direction a company will take in the months ahead. With Q1 behind us, let’s have a look at Universal Technical Institute (NYSE: UTI) and its peers.

A whole industry has emerged to address the problem of rising education costs, offering consumers alternatives to traditional education paths such as four-year colleges. These alternative paths, which may include online courses or flexible schedules, make education more accessible to those with work or child-rearing obligations. However, some have run into issues around the value of the degrees and certifications they provide and whether customers are getting a good deal. Those who don’t prove their value could struggle to retain students, or even worse, invite the heavy hand of regulation.

The 8 education services stocks we track reported a very strong Q1. As a group, revenues beat analysts’ consensus estimates by 2.3% while next quarter’s revenue guidance was in line.

Luckily, education services stocks have performed well with share prices up 10.4% on average since the latest earnings results.

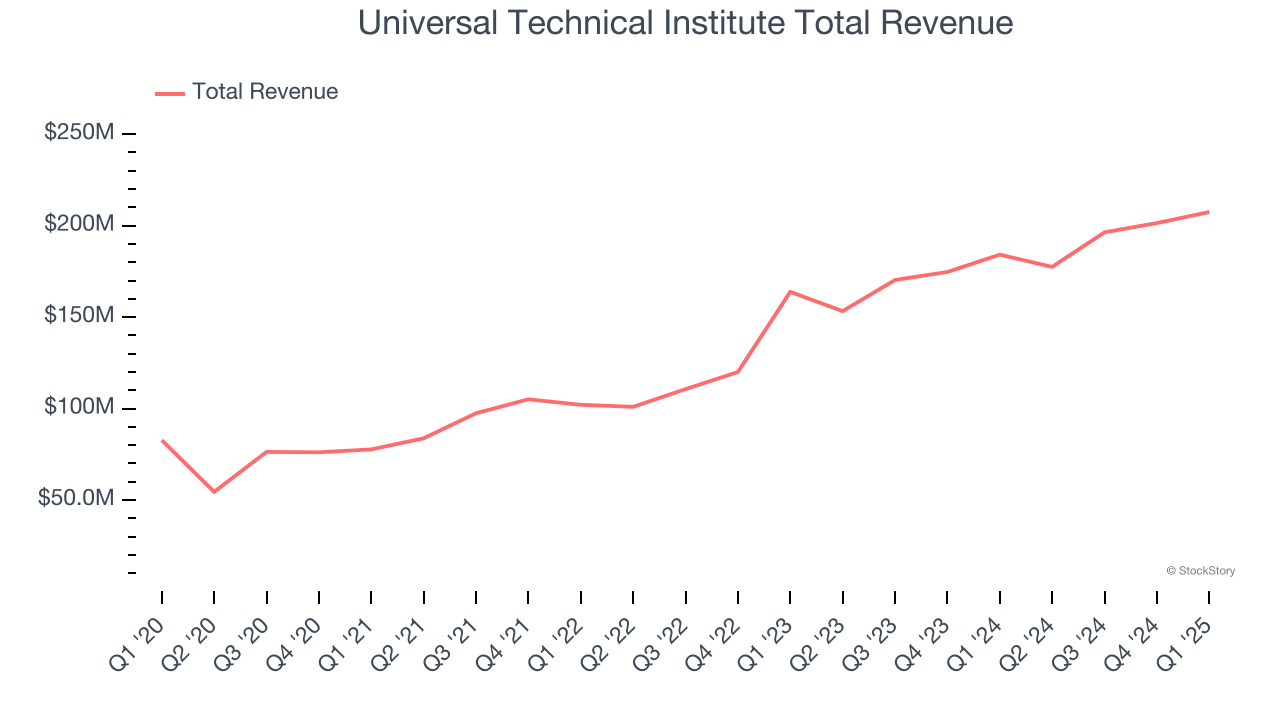

Universal Technical Institute (NYSE: UTI)

Founded in 1965, Universal Technical Institute (NYSE: UTI) is a leading provider of technical training programs, specializing in automotive, diesel, collision repair, motorcycle, and marine technicians.

Universal Technical Institute reported revenues of $207.4 million, up 12.6% year on year. This print exceeded analysts’ expectations by 2.8%. Overall, it was an exceptional quarter for the company with an impressive beat of analysts’ EPS estimates and a solid beat of analysts’ EBITDA estimates.

"We delivered another strong quarter in Q2 as we continued to advance our North Star Strategy and build on our operational momentum," said Jerome Grant, CEO of Universal Technical Institute, Inc.

Universal Technical Institute achieved the highest full-year guidance raise of the whole group. Unsurprisingly, the stock is up 18.4% since reporting and currently trades at $35.08.

Is now the time to buy Universal Technical Institute? Access our full analysis of the earnings results here, it’s free.

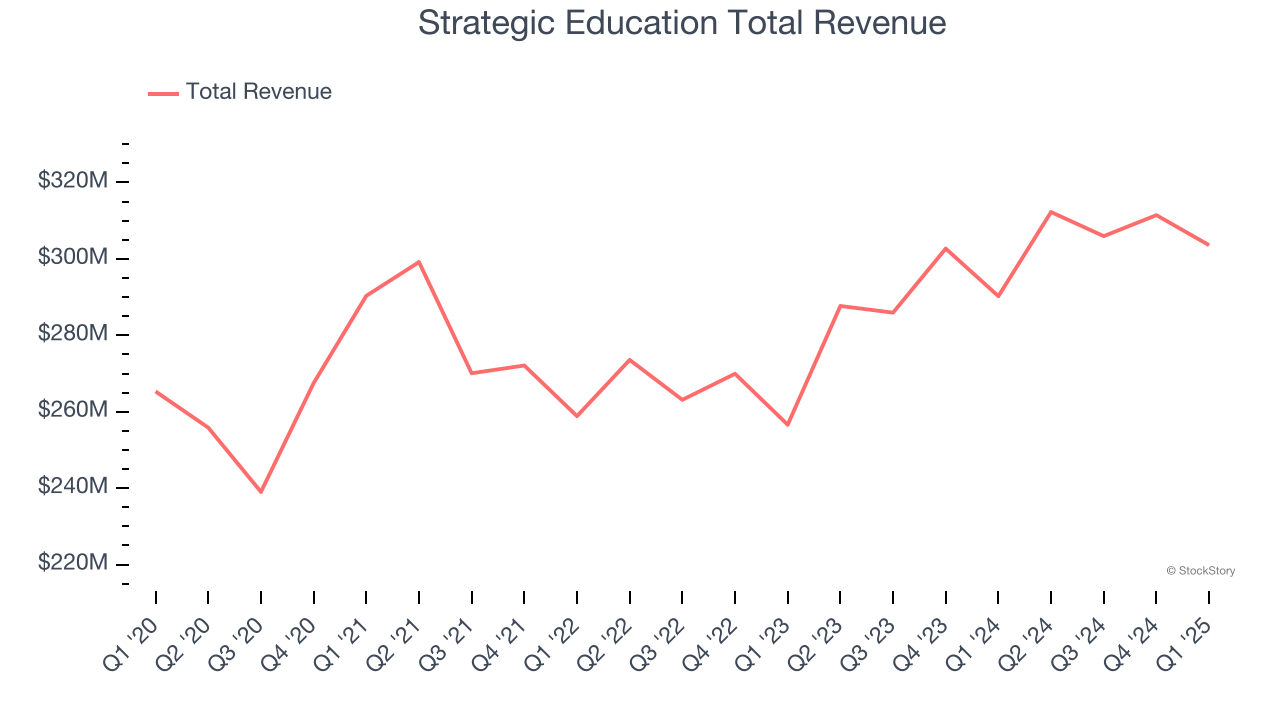

Best Q1: Strategic Education (NASDAQ: STRA)

Formed through the merger of Strayer Education and Capella Education in 2018, Strategic Education (NASDAQ: STRA) is a career-focused higher education provider.

Strategic Education reported revenues of $303.6 million, up 4.6% year on year, outperforming analysts’ expectations by 1%. The business had an exceptional quarter with a solid beat of analysts’ EPS estimates and an impressive beat of analysts’ adjusted operating income estimates.

The market seems happy with the results as the stock is up 9% since reporting. It currently trades at $87.47.

Is now the time to buy Strategic Education? Access our full analysis of the earnings results here, it’s free.

Slowest Q1: Grand Canyon Education (NASDAQ: LOPE)

Founded in 1949, Grand Canyon Education (NASDAQ: LOPE) is an educational services provider known for its operation at Grand Canyon University.

Grand Canyon Education reported revenues of $289.3 million, up 5.3% year on year, exceeding analysts’ expectations by 0.8%. It was a satisfactory quarter as it also posted EPS guidance for next quarter exceeding analysts’ expectations but a miss of analysts’ students estimates.

Interestingly, the stock is up 5.3% since the results and currently trades at $195.20.

Read our full analysis of Grand Canyon Education’s results here.

Bright Horizons (NYSE: BFAM)

Founded in 1986, Bright Horizons (NYSE: BFAM) is a global provider of child care, early education, and workforce support solutions.

Bright Horizons reported revenues of $665.5 million, up 6.9% year on year. This number met analysts’ expectations. Overall, it was a strong quarter as it also produced an impressive beat of analysts’ adjusted operating income estimates and a solid beat of analysts’ EPS estimates.

Bright Horizons had the weakest performance against analyst estimates among its peers. The stock is up 2.3% since reporting and currently trades at $129.62.

Read our full, actionable report on Bright Horizons here, it’s free.

Perdoceo Education (NASDAQ: PRDO)

Formerly known as Career Education Corporation, Perdoceo Education (NASDAQ: PRDO) is an educational services company that specializes in postsecondary education.

Perdoceo Education reported revenues of $213 million, up 26.6% year on year. This result beat analysts’ expectations by 2.4%. It was a strong quarter as it also recorded EPS guidance for next quarter exceeding analysts’ expectations.

Perdoceo Education delivered the fastest revenue growth among its peers. The stock is up 23.3% since reporting and currently trades at $31.03.

Read our full, actionable report on Perdoceo Education here, it’s free.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our Strong Momentum Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.