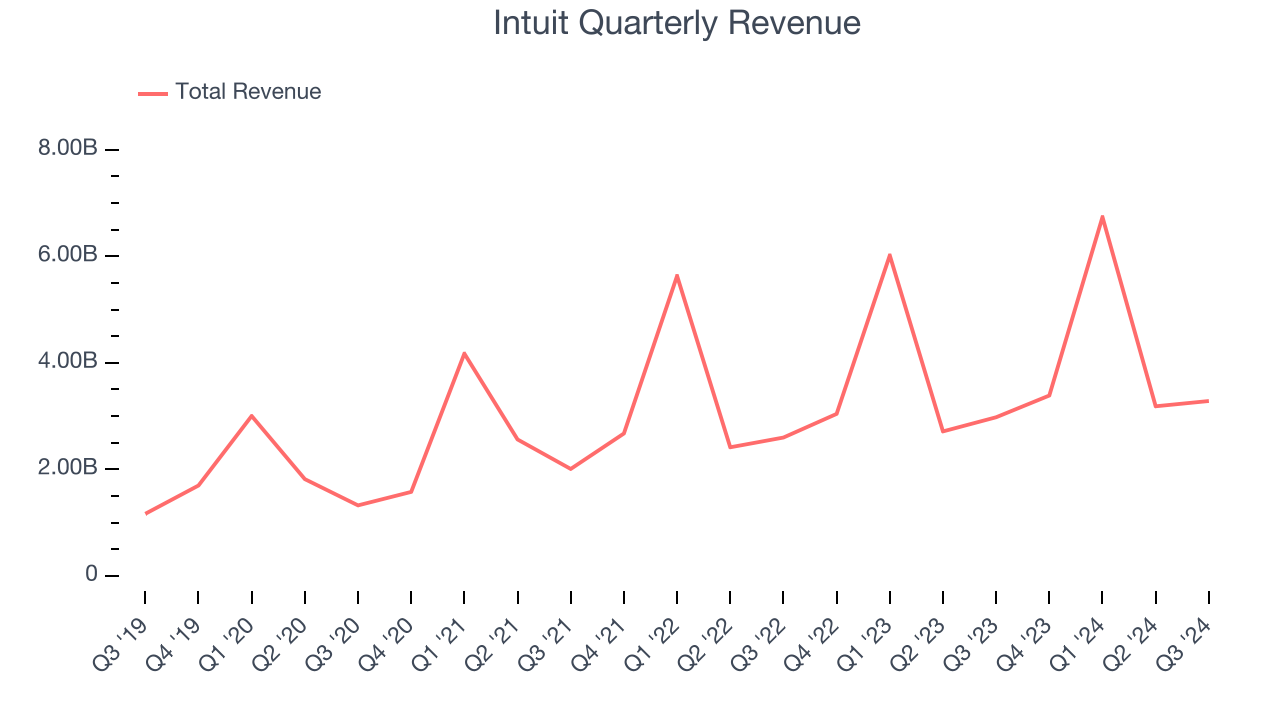

Tax and accounting software provider, Intuit (NASDAQ:INTU) reported Q3 CY2024 results exceeding the market’s revenue expectations, with sales up 10.2% year on year to $3.28 billion. On the other hand, next quarter’s revenue guidance of $3.83 billion was less impressive, coming in 1.3% below analysts’ estimates. Its non-GAAP profit of $2.50 per share was 6% above analysts’ consensus estimates.

Is now the time to buy Intuit? Find out by accessing our full research report, it’s free.

Intuit (INTU) Q3 CY2024 Highlights:

- Revenue: $3.28 billion vs analyst estimates of $3.14 billion (10.2% year-on-year growth, 4.6% beat)

- Adjusted EPS: $2.50 vs analyst estimates of $2.36 (6% beat)

- Adjusted Operating Income: $953 million vs analyst estimates of $899.2 million (29% margin, 6% beat)

- The company reconfirmed its revenue guidance for the full year of $18.25 billion at the midpoint

- Management reiterated its full-year Adjusted EPS guidance of $19.26 at the midpoint

- Operating Margin: 8.3%, down from 10.3% in the same quarter last year

- Free Cash Flow Margin: 10%, down from 11.8% in the previous quarter

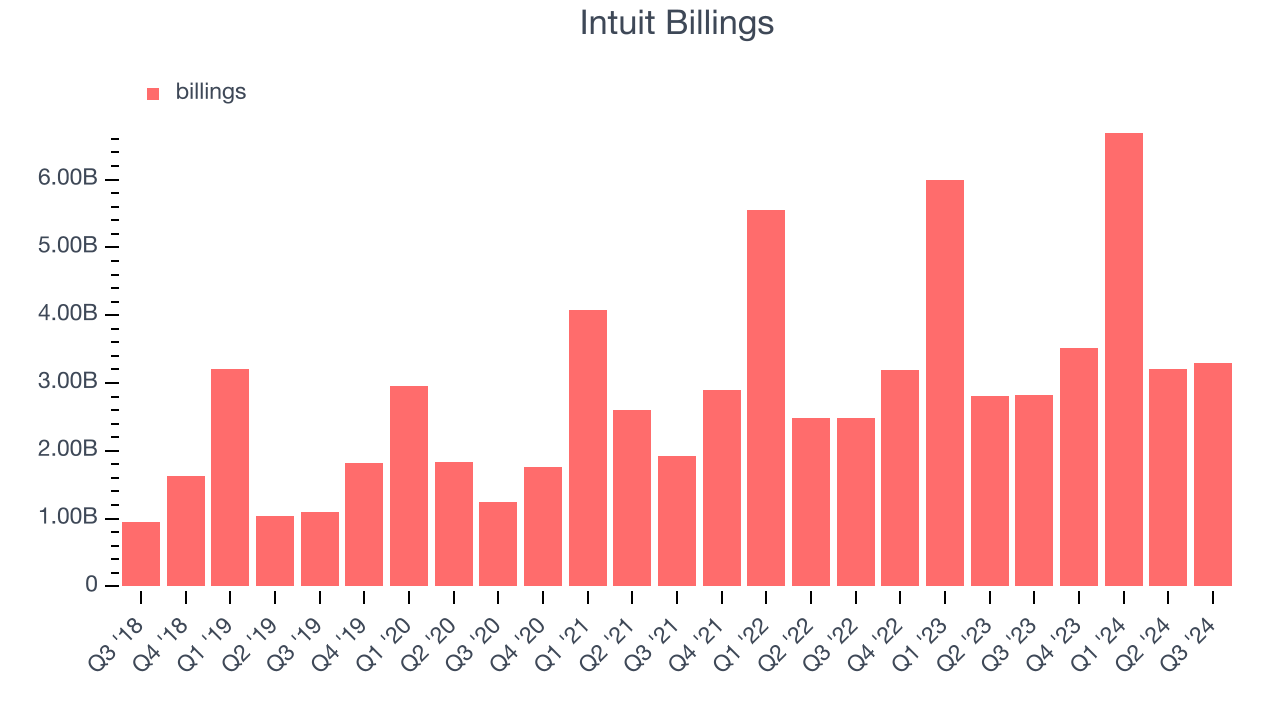

- Billings: $3.30 billion at quarter end, up 17.1% year on year

- Market Capitalization: $182.4 billion

"We've had a strong start to the year as we demonstrate the power of Intuit's AI-driven expert platform strategy. By delivering 'done-for-you' experiences, enabled by AI with access to AI-powered human experts, we continue to fuel the success of consumers and businesses," said Sasan Goodarzi, Intuit's CEO.

Company Overview

Created in 1983 when founder Scott Cook watched his wife struggle to reconcile the family's checkbook, Intuit provides tax and accounting software for small and medium-sized businesses.

Tax Software

The demand for easy to use, integrated cloud based finance software that integrates tax and accounting operations continues to rise in tandem with the difficulty workers find trying to use existing accounting tools like spreadsheets given the growing volume of finance data littered across a multitude of enterprise applications. A related demand driver is the secular increase of e-commerce and rising adoption of modern point of sales and payments platforms which easily integrate with backend financial software.

Sales Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Over the last three years, Intuit grew its sales by 17.2% annually. Although this growth is solid on an absolute basis, it fell slightly short of our benchmark for the software sector. Luckily, there are other things to like about Intuit.

This quarter, Intuit reported year-on-year revenue growth of 10.2%, and its $3.28 billion of revenue exceeded Wall Street’s estimates by 4.6%. Company management is currently guiding for a 13.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 12.8% over the next 12 months, a deceleration versus the last three years. We still think its growth trajectory is satisfactory and implies the market is baking in success for its products and services. Some tapering/deceleration is natural given the magnitude of its revenue base.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Billings

In addition to revenue, billings is a non-GAAP metric that sheds additional light on Intuit’s business quality. Billings is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Intuit’s billings punched in at $3.30 billion in the latest quarter, and over the last four quarters, its growth slightly outpaced the sector as it averaged 13.3% year-on-year increases. This performance was in line with its total sales growth and shows the company is successfully converting sales into cash. Its growth also enhances liquidity and provides a solid foundation for future investments.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Intuit is extremely efficient at acquiring new customers, and its CAC payback period checked in at 12.7 months this quarter. The company’s performance indicates it has a highly differentiated product offering and a strong brand reputation that comes from scale. These dynamics give Intuit the freedom to invest in new product initiatives while maintaining optionality.

Key Takeaways from Intuit’s Q3 Results

We were impressed by how significantly Intuit blew past analysts’ billings and EPS expectations this quarter. On the other hand, its revenue guidance for next quarter fell short of Wall Street's estimates and its EPS guidance missed by even more. Overall, this was a softer quarter. The stock traded down 6.2% to $637 immediately after reporting.

The latest quarter from Intuit’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.