EVgo’s stock price has taken a beating over the past six months, shedding 32.2% of its value and falling to $2.80 per share. This might have investors contemplating their next move.

Is there a buying opportunity in EVgo, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Even with the cheaper entry price, we're cautious about EVgo. Here are three reasons why there are better opportunities than EVGO and a stock we'd rather own.

Why Is EVgo Not Exciting?

Created through a settlement between NRG Energy and the California Public Utilities Commission, EVgo (NASDAQ: EVGO) is a provider of electric vehicle charging solutions, operating fast charging stations across the United States.

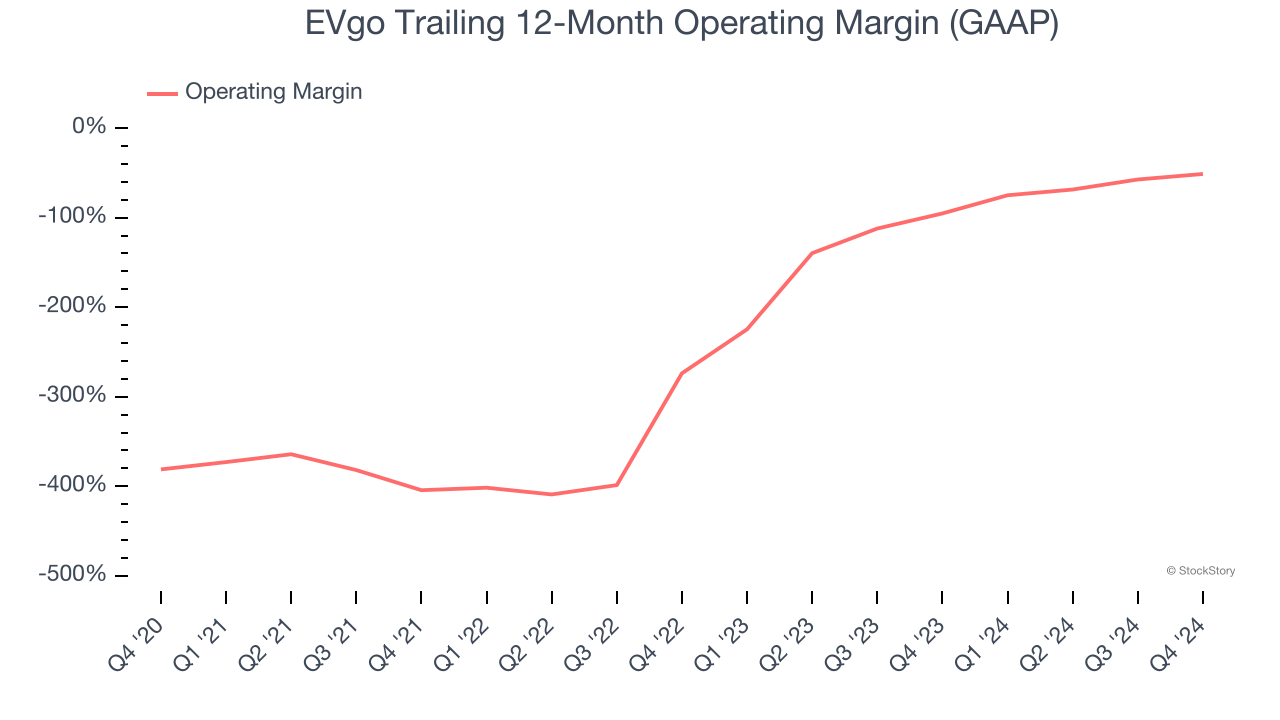

1. Operating Losses Sound the Alarms

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

EVgo’s high expenses have contributed to an average operating margin of negative 114% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It’s hard to trust that the business can endure a full cycle.

2. Cash Burn Ignites Concerns

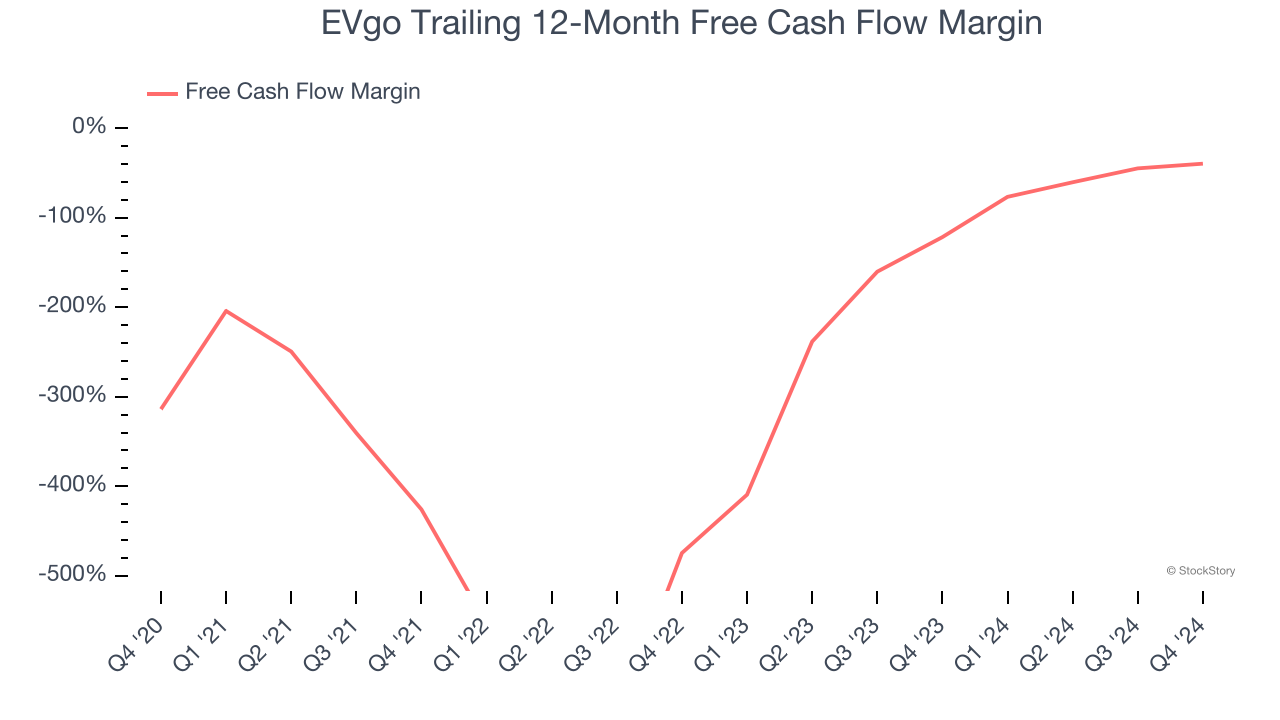

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

EVgo’s demanding reinvestments have drained its resources over the last five years, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 137%, meaning it lit $136.97 of cash on fire for every $100 in revenue.

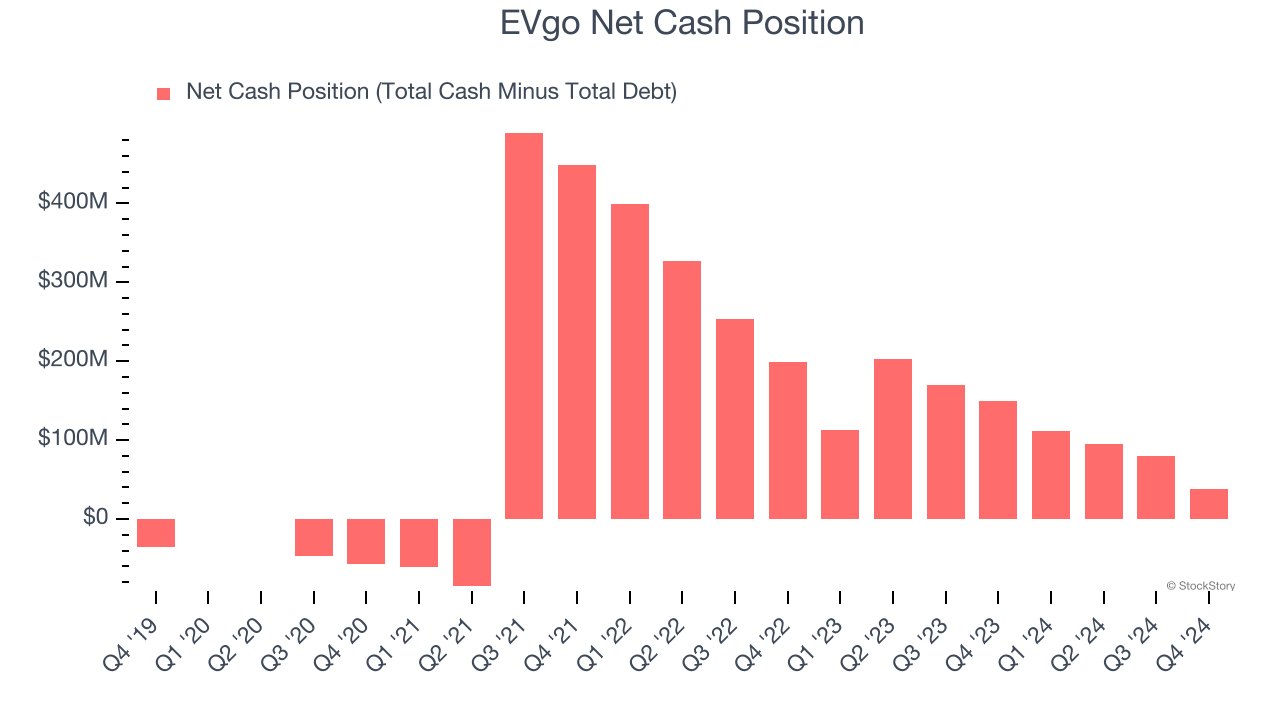

3. Short Cash Runway Exposes Shareholders to Potential Dilution

As long-term investors, the risk we care about most is the permanent loss of capital, which can happen when a company goes bankrupt or raises money from a disadvantaged position. This is separate from short-term stock price volatility, something we are much less bothered by.

EVgo burned through $102 million of cash over the last year. With $120.5 million of cash on its balance sheet, the company has around 14 months of runway left (assuming its $82.82 million of debt isn’t due right away).

Unless the EVgo’s fundamentals change quickly, it might find itself in a position where it must raise capital from investors to continue operating. Whether that would be favorable is unclear because dilution is a headwind for shareholder returns.

We remain cautious of EVgo until it generates consistent free cash flow or any of its announced financing plans materialize on its balance sheet.

Final Judgment

EVgo’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 179.6× forward EV-to-EBITDA (or $2.80 per share). Beauty is in the eye of the beholder, but we don’t really see a big opportunity at the moment. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at a dominant Aerospace business that has perfected its M&A strategy.

Stocks We Would Buy Instead of EVgo

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Sterling Infrastructure (+1,096% five-year return). Find your next big winner with StockStory today for free.