- SECURE 2.0 is a step in the right direction, but small changes to retirement plans could go a long way toward promoting retirement security.

- Four out of ten defined contribution plan participants say they don’t save more for retirement because “Inflation is eating up too much of my paycheck.”

- Seven out of ten workers think Social Security benefits will be dramatically reduced when they retire; a majority favor mandates that go beyond SECURE 2.0, including universal access to retirement savings plans, mandatory company matches, and individual contributions.

- Most employees, including nine out of ten millennials and nearly half of baby boomers, say they would save more – or begin to save – if sustainable investments were available in their company-sponsored retirement plans. Most also want access to income-generating investments (90%); alternatives (77%) and cryptocurrency (52%, including 78% of millennials).

- One-third of millennials get their retirement investment advice from TikTok, Twitter, and other social media groups. Nearly half say recent market volatility taught them the value of professional advice.

If the key to a financially secure retirement is to save big and start early, millennials are doing a lot right, in part because of provisions in retirement plan design, such as automatic enrollment of new employees, to help more American workers reach their retirement goals. A new survey by Natixis Investment Managers (Natixis IM) found that millennials started saving for retirement 11 years earlier in life than baby boomers did, and they are contributing a whopping 16% of their annual salaries toward it, on average.

This press release features multimedia. View the full release here: https://www.businesswire.com/news/home/20230418005492/en/

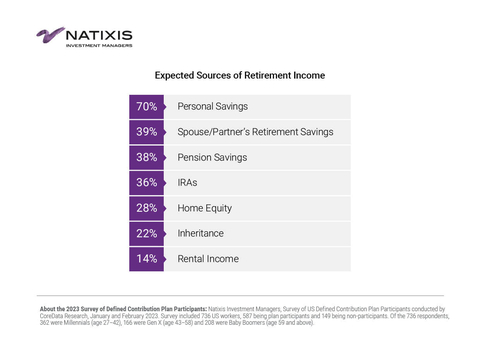

Expected Sources of Retirement Income (Graphic: Business Wire)

The survey shows that further expansion of retirement plan provisions, codified by recent passage of the SECURE 2.0 retirement act, strongly resonates with employees amid considerable changes in retirement expectations, financial conditions, and workforce demographics.

“American workers are feeling the weight of responsibility for retirement funding, and younger generations, in particular, are pushing for changes that will better meet their distinct needs and preferences,” said Liana Magner, Head of Retirement and Institutional in the US for Natixis Investment Managers. “Making retirement savings easy and appealing and helping them stay on track, particularly during periods of financial stress, will take united efforts from employers, individuals, and policymakers.”

The survey found serious shortfalls in retirement savings, especially among baby boomers, of whom 58% say their biggest regret is that they didn’t start saving sooner. While millennials have time on their side, the financial headwinds they are facing at a crucial stage of life threaten to derail their progress.

- Inflation is the Number One barrier to saving more for retirement, a financial stressor cited by the largest percentage of respondents across all generations (44%). For millennials, competing financial goals rank as a close Number Two.

- One in four (25%) defined contribution plan participants, including 38% of millennials, took an early withdrawal from their plan in the past 12 months. The three top reasons millennials tapped their savings were to cover healthcare costs (41%), home repairs (36%), and debt repayment (34%).

- 83% of millennials and 78% of Generation X think Social Security benefits will be dramatically reduced by the time they retire.

- Just 46% of millennials—half as many as baby boomers (90%)—are even factoring Social Security into their retirement income planning. More so than any other generation, millennials are looking beyond traditional sources of retirement income (pension, Social Security, defined contribution plan) to fund their retirement. They plan to use all available sources, including equity in their homes (29%), inheritance (24%), rental income (19%), sale of a business (19%), and support from their children (19%).

“It’s gotten a lot harder in the past two years for people to generate the personal savings that will ground their retirement income plans. It’s gotten to the point where one in five millennials, the generation that started out living in their parents’ basement, now think they might end up in their kids’ garage,” said Dave Goodsell, Executive Director of the Natixis Center for Investor Insight. “To adapt to today’s complex financial environment, employers should adapt their retirement plan benefit design and tailor their investment offering around the evolving needs of a multi-generational workforce.”

Recent Policy Changes Are a Step in the Right Direction

The survey suggests that provisions put in place by SECURE 2.0 will be a positive step in the right direction once they go into effect. Among these provisions are automatic enrollment in company-sponsored DC plans with default investment options known as Qualified Default Investment Alternatives (QDIA); recognition of student loan repayments to qualify for employer matches; linked emergency savings accounts; and higher catch-up contribution limits for older workers. The survey found:

- 42% of workers who do not contribute now, including 63% of millennials, say they will begin to participate in their company plan when student loan payment matching benefits take effect.

- 54% of non-participants, including 77% of millennials, intend to participate if linked emergency savings features become available.

- 31% of millennials who participate now were automatically enrolled, and 40% still hold the default investments initially selected for them.

A second, separate ruling, the US Department of Labor’s Prudence and Loyalty in Selecting Plan Investments and Exercising Shareholder Rights, adds another critical incentive to the mix: consideration of participant preferences when constructing a menu of investment options. According to the survey findings, DC plan participants show a remarkably high level of interest and engagement around ESG (environmental, social and governance) issues and sustainable investments.

- Most (83%) of respondents believe companies that focus on sustainable business practices present significant opportunities for growth.

- 73% of all survey respondents—including 88% of millennials, 72% of Generation X, and as many as 49% of baby boomers—said they would be more likely to participate in their company DC plan or increase their contributions if they were offered investments in companies with good environment, social and governance practices.

What Employers Can Do: Give employees what they want with a range of options that matter

With mandates taking effect, employers will need to focus on their Qualified Default Investment Alternative, overall investment offering, educational support, and guidance for their employees.

- Plan participants want to see a range of investment options available in their plans, including retirement income-generating investments (90%); alternatives (77%), and sustainability-focused options (82%, including 92% of millennials). Half (52%) want access to cryptocurrency in their retirement plan offering, including 78% of millennials.

- 41% of all respondents say that access to professional investment advice would be a top incentive for them to contribute more to their retirement plan. Nearly one-third (32%) of millennials presently get their investment advice from social media, including TikTok, Twitter, and Facebook, and 46% scour the Internet for insight. Almost half (47%) of millennials and 39% of respondents overall say recent volatility convinced them of the need for professional investment advice.

- 67% of plan participants say a bigger company match would be the top reason for contributing more to their retirement plan. The company match was the Number One reason for deciding to participate in the plan for all respondents except millennials, who say the convenience of automatic paycheck withdrawal is the biggest reason they initially joined.

Matching contributions may also be an effective lever for employers in a tight labor market. While respondents report an average maximum company match of 7.8%, millennials are most likely to work for a company that offers greater than a 10% match (31%). More than half (54%) of millennials and 43% of respondents overall say their employer increased the company’s match in the past 12 months.

The majority of those surveyed, particularly millennials, also are open to policy changes that would demand more from employers, financial services providers, individuals and the government alike.

- 67% of respondents overall, including 85% of millennials, believe it is the government’s responsibility to provide universal access to a retirement savings plan.

- 81%, including 88% of millennials, think employers should be required to offer retirement plans.

- 78%, including 87% of millennials, believe employer matching contributions should be mandatory.

- 69%, including 82% of millennials, say individuals should be required to make contributions toward their retirement savings.

A copy of the report with analysis and findings from the Natixis Investment Managers 2023 Survey of Defined Contribution Plan Participants/Non-Participants can be found at: https://im.natixis.com/us/research/2023-defined-contribution-plan-participant-survey

Methodology

Natixis IM surveyed 736 US workers, all of whom have access to a company-sponsored defined contribution (DC) retirement savings plan, such as a 401(k), 403(b), 457, SIMPLE IRA or SEP. The survey, conducted by CoreData Research in January and February 2023, looked at behavior, preferences and attitudes about retirement savings across three generations including millennials (ages 27 to 42), Generation X (ages 43 to 58) and baby boomers (age 59 and above).

About Natixis Investment Managers

Natixis Investment Managers’ multi-affiliate approach connects clients to the independent thinking and focused expertise of more than 15 active managers. Ranked among the world’s largest asset managers1 with more than $1 trillion assets under management2 (€1 trillion), Natixis Investment Managers delivers a diverse range of solutions across asset classes, styles, and vehicles, including innovative environmental, social, and governance (ESG) strategies and products dedicated to advancing sustainable finance. The firm partners with clients in order to understand their unique needs and provide insights and investment solutions tailored to their long-term goals.

Headquartered in Paris and Boston, Natixis Investment Managers is part of the Global Financial Services division of Groupe BPCE, the second-largest banking group in France through the Banque Populaire and Caisse d’Epargne retail networks. Natixis Investment Managers’ affiliated investment management firms include AEW; DNCA Investments;3 Dorval Asset Management; Flexstone Partners; Gateway Investment Advisers; Harris Associates; Investors Mutual Limited; Loomis, Sayles & Company; Mirova; MV Credit; Naxicap Partners; Ossiam; Ostrum Asset Management; Seventure Partners; Thematics Asset Management; Vauban Infrastructure Partners; Vaughan Nelson Investment Management; and WCM Investment Management. Additionally, investment solutions are offered through Natixis Investment Managers Solutions and Natixis Advisors, LLC. Not all offerings are available in all jurisdictions. For additional information, please visit Natixis Investment Managers’ website at im.natixis.com | LinkedIn: linkedin.com/company/natixis-investment-managers.

Natixis Investment Managers’ distribution and service groups include Natixis Distribution, LLC, a limited purpose broker-dealer and the distributor of various U.S. registered investment companies for which advisory services are provided by affiliated firms of Natixis Investment Managers, Natixis Investment Managers S.A. (Luxembourg), Natixis Investment Managers International (France), and their affiliated distribution and service entities in Europe and Asia.

1 Cerulli Quantitative Update: Global Markets 2022 ranked Natixis Investment Managers as the 18th largest asset manager in the world based on assets under management as of December 31, 2021.

2 Assets under management (“AUM”) of affiliated entities measured as of December 31, 2022 are $1,151.3 billion (€1,078.8 billion). AUM includes AlphaSimplex Group, LLC ($8.2 billion / €7.7 billion), which was acquired by Virtus Investment Partners, Inc., effective April 1, 2023. AUM, as reported, may include notional assets, assets serviced, gross assets, assets of minority-owned affiliated entities and other types of non-regulatory AUM managed or serviced by firms affiliated with Natixis Investment Managers.

3 A brand of DNCA Finance.

5624713.1.1

View source version on businesswire.com: https://www.businesswire.com/news/home/20230418005492/en/

Contacts

Press:

Kelly Cameron

+1 617-449-2543

Kelly.Cameron@natixis.com