Teladoc has been treading water for the past six months, recording a small return of 2.5% while holding steady at $8.62.

Is now the time to buy Teladoc, or should you be careful about including it in your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

We're swiping left on Teladoc for now. Here are three reasons why TDOC doesn't excite us and a stock we'd rather own.

Why Is Teladoc Not Exciting?

Founded to help people in rural areas get online medical consultations, Teladoc Health (NYSE: TDOC) is a telemedicine platform that facilitates remote doctor’s visits.

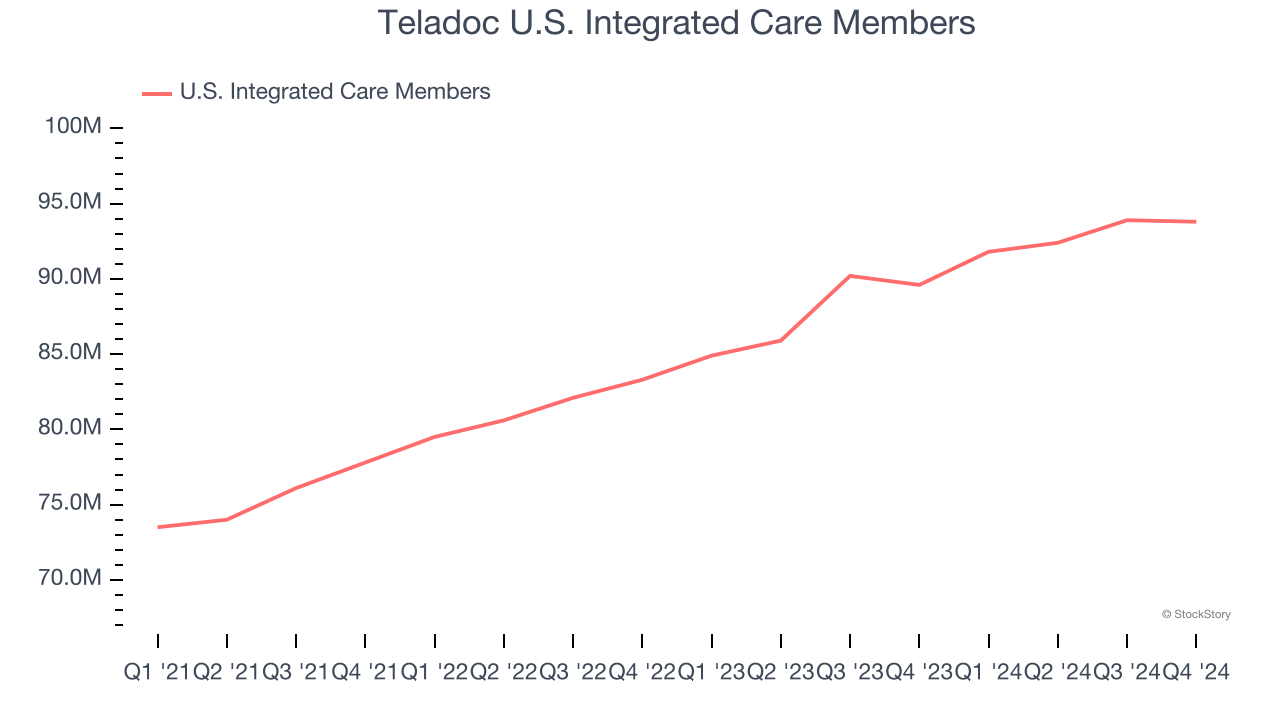

1. Change in U.S. Integrated Care Members Points to Soft Demand

As an online marketplace, Teladoc generates revenue growth by increasing both the number of users on its platform and the average order size in dollars.

Over the last two years, Teladoc’s u.s. integrated care members, a key performance metric for the company, increased by 6.9% annually to 93.8 million in the latest quarter. This growth rate is slightly below average for a consumer internet business. If Teladoc wants to reach the next level, it likely needs to enhance the appeal of its current offerings or innovate with new products.

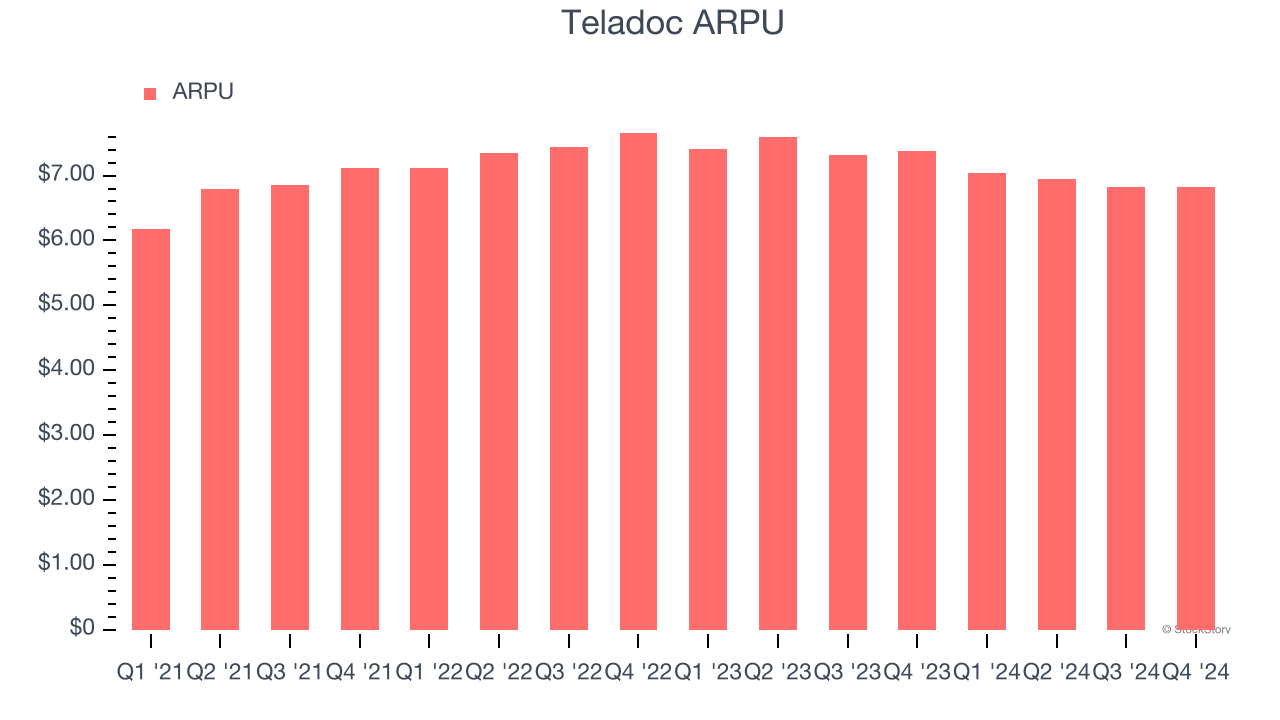

2. Customer Spending Decreases, Engagement Falling?

Average revenue per user (ARPU) is a critical metric to track because it measures how much the company earns in transaction fees from each user. ARPU also gives us unique insights into a user’s average order size and Teladoc’s take rate, or "cut", on each order.

Teladoc’s ARPU fell over the last two years, averaging 3.2% annual declines. This isn’t great when combined with its weaker u.s. integrated care members performance. If Teladoc tries boosting ARPU by taking a more aggressive approach to monetization, it’s unclear whether user growth would be sustainable.

3. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Teladoc’s revenue to drop by 2.1%, a decrease from its 8.1% annualized growth for the past three years. This projection doesn't excite us and indicates its products and services will face some demand challenges.

Final Judgment

Teladoc isn’t a terrible business, but it doesn’t pass our quality test. That said, the stock currently trades at 4.6× forward EV-to-EBITDA (or $8.62 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are more exciting stocks to buy at the moment. We’d suggest looking at an all-weather company that owns household favorite Taco Bell.

Stocks We Would Buy Instead of Teladoc

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.