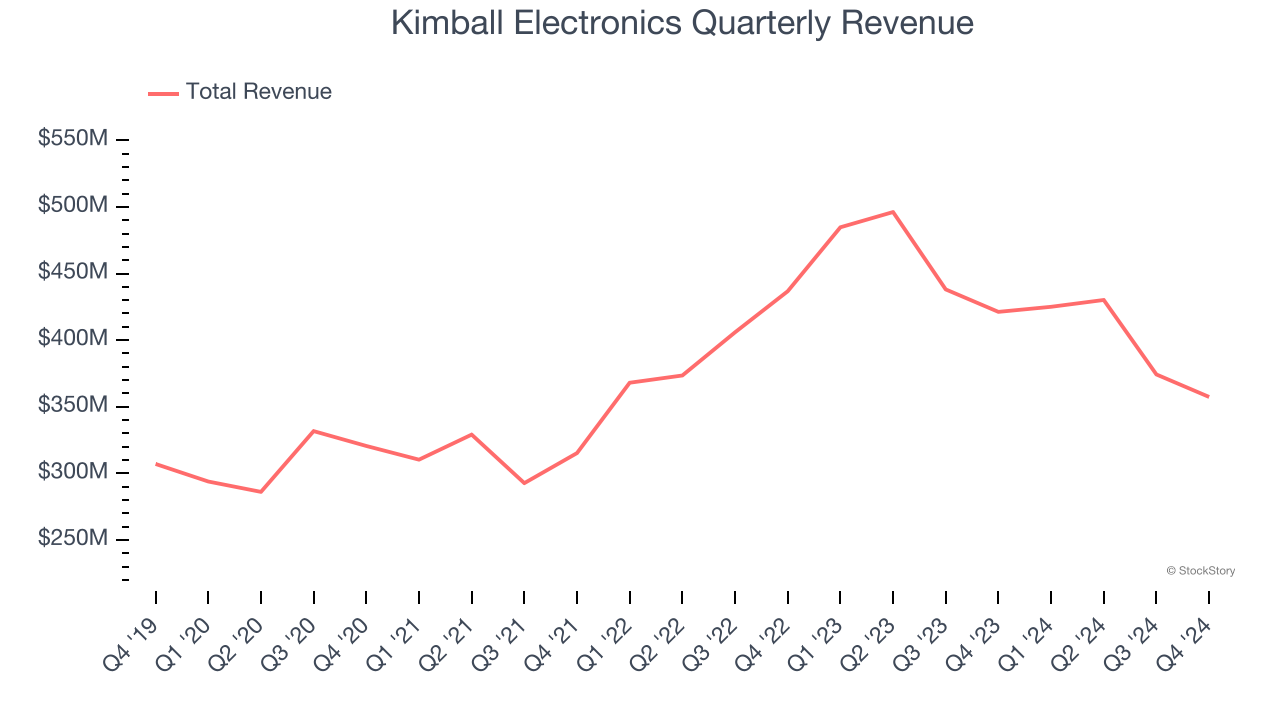

Global electronics contract manufacturer Kimball Electronics (NYSE: KE) missed Wall Street’s revenue expectations in Q4 CY2024, with sales falling 15.2% year on year to $357.4 million. The company’s full-year revenue guidance of $1.42 billion at the midpoint came in 4.4% below analysts’ estimates. Its non-GAAP profit of $0.29 per share was 28.9% above analysts’ consensus estimates.

Is now the time to buy Kimball Electronics? Find out by accessing our full research report, it’s free.

Kimball Electronics (KE) Q4 CY2024 Highlights:

- Revenue: $357.4 million vs analyst estimates of $360.1 million (15.2% year-on-year decline, 0.7% miss)

- Adjusted EPS: $0.29 vs analyst estimates of $0.23 (28.9% beat)

- The company dropped its revenue guidance for the full year to $1.42 billion at the midpoint from $1.49 billion, a 4.7% decrease

- Operating Margin: 2.3%, down from 4.1% in the same quarter last year

- Market Capitalization: $432.7 million

Commenting on today’s announcement, Richard D. Phillips, Chief Executive Officer, stated, “The results for the second quarter were in line with expectations as we continue to navigate a sustained period of declining customer demand, while focusing on what is controllable. For the fourth consecutive quarter, cash flow generated from operating activities was positive, inventory levels were reduced, and debt was paid down, with borrowings nearly 40% lower than a year ago. Our improved balance sheet provides ample liquidity to weather our current challenges, along with the necessary dry powder to opportunistically and meaningfully invest in growing the business.”

Company Overview

Founded in 1961, Kimball Electronics (NYSE: KE) is a global contract manufacturer specializing in electronics and manufacturing solutions for automotive, medical, and industrial markets.

Electrical Systems

Like many equipment and component manufacturers, electrical systems companies are buoyed by secular trends such as connectivity and industrial automation. More specific pockets of strong demand include Internet of Things (IoT) connectivity and the 5G telecom upgrade cycle, which can benefit companies whose cables and conduits fit those needs. But like the broader industrials sector, these companies are also at the whim of economic cycles. Interest rates, for example, can greatly impact projects that drive demand for these products.

Sales Growth

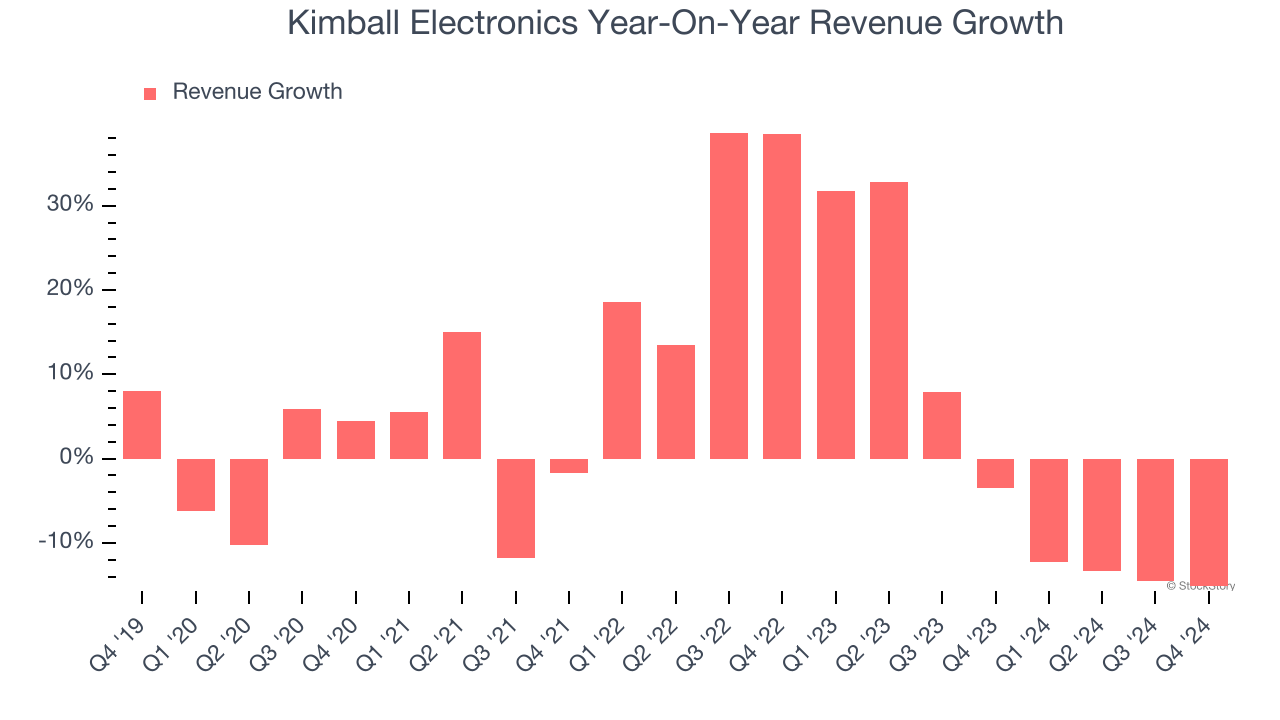

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Regrettably, Kimball Electronics’s sales grew at a tepid 4.8% compounded annual growth rate over the last five years. This was below our standard for the industrials sector and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Kimball Electronics’s recent history shows its demand slowed as its revenue was flat over the last two years.

This quarter, Kimball Electronics missed Wall Street’s estimates and reported a rather uninspiring 15.2% year-on-year revenue decline, generating $357.4 million of revenue.

Looking ahead, sell-side analysts expect revenue to decline by 5.6% over the next 12 months, a deceleration versus the last two years. This projection is underwhelming and implies its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Adjusted Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

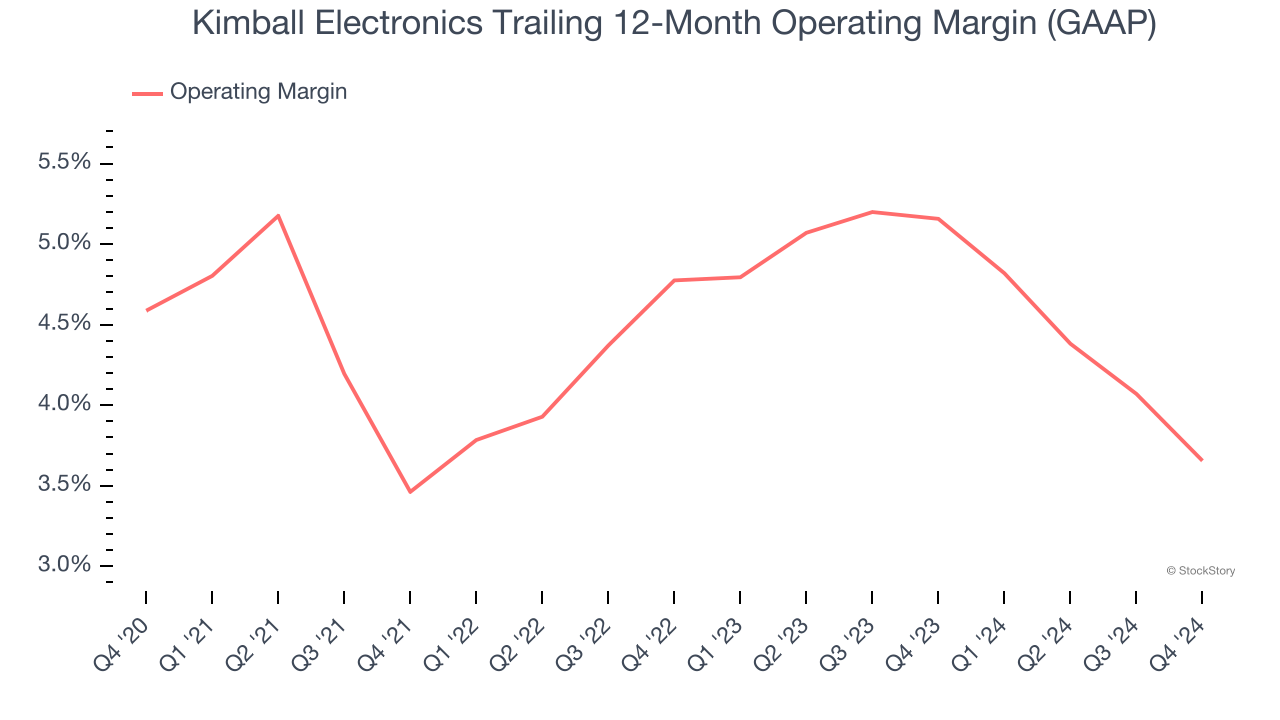

Kimball Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.4% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Kimball Electronics’s operating margin might have seen some fluctuations but has generally stayed the same over the last five years, which doesn’t help its cause.

In Q4, Kimball Electronics generated an operating profit margin of 2.3%, down 1.8 percentage points year on year. Since Kimball Electronics’s operating margin decreased more than its gross margin, we can assume it was recently less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

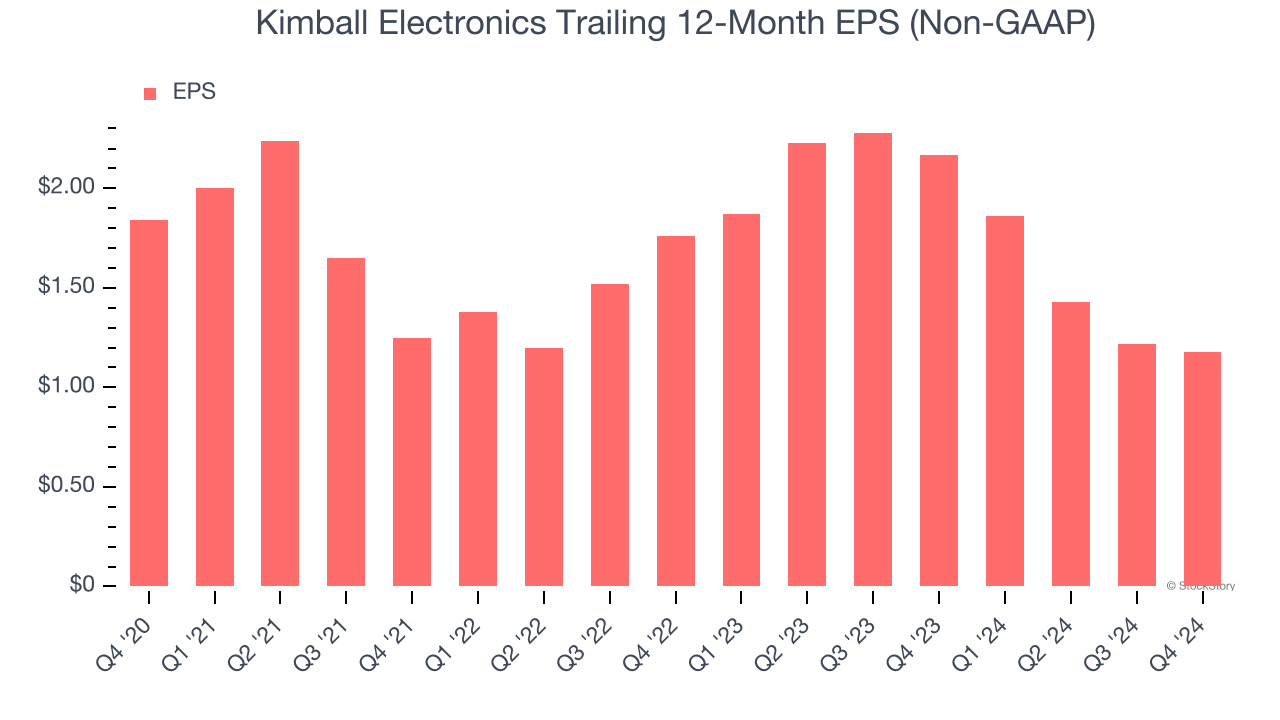

Kimball Electronics’s full-year EPS dropped 49.2%, or 10.5% annually, over the last four years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Kimball Electronics’s low margin of safety could leave its stock price susceptible to large downswings.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Kimball Electronics, its EPS declined by 18.1% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

We can take a deeper look into Kimball Electronics’s earnings to better understand the drivers of its performance. Kimball Electronics’s operating margin has declined by 2 percentage points over the last two years. This was the most relevant factor (aside from the revenue impact) behind its lower earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

In Q4, Kimball Electronics reported EPS at $0.29, down from $0.33 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Kimball Electronics’s full-year EPS of $1.18 to grow 32.6%.

Key Takeaways from Kimball Electronics’s Q4 Results

Kimball Electronics's revenue in the quarter missed. Adding to the bad news was the company's lowering of its full-year revenue and operating margin guidance, which fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 4.5% to $17.06 immediately after reporting.

Kimball Electronics’s earnings report left more to be desired. Let’s look forward to see if this quarter has created an opportunity to buy the stock. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.