What a fantastic six months it’s been for Twilio. Shares of the company have skyrocketed 96.9%, hitting $111.06. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Twilio, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons why you should be careful with TWLO and a stock we'd rather own.

Why Is Twilio Not Exciting?

Founded in 2008 by Jeff Lawson, a former engineer at Amazon, Twilio (NYSE: TWLO) is a software as a service platform that makes it really easy for software developers to use text messaging, voice calls and other forms of communication in their apps.

1. Weak Billings Point to Soft Demand

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Twilio’s billings came in at $1.13 billion in Q3, and over the last four quarters, its year-on-year growth averaged 5.3%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

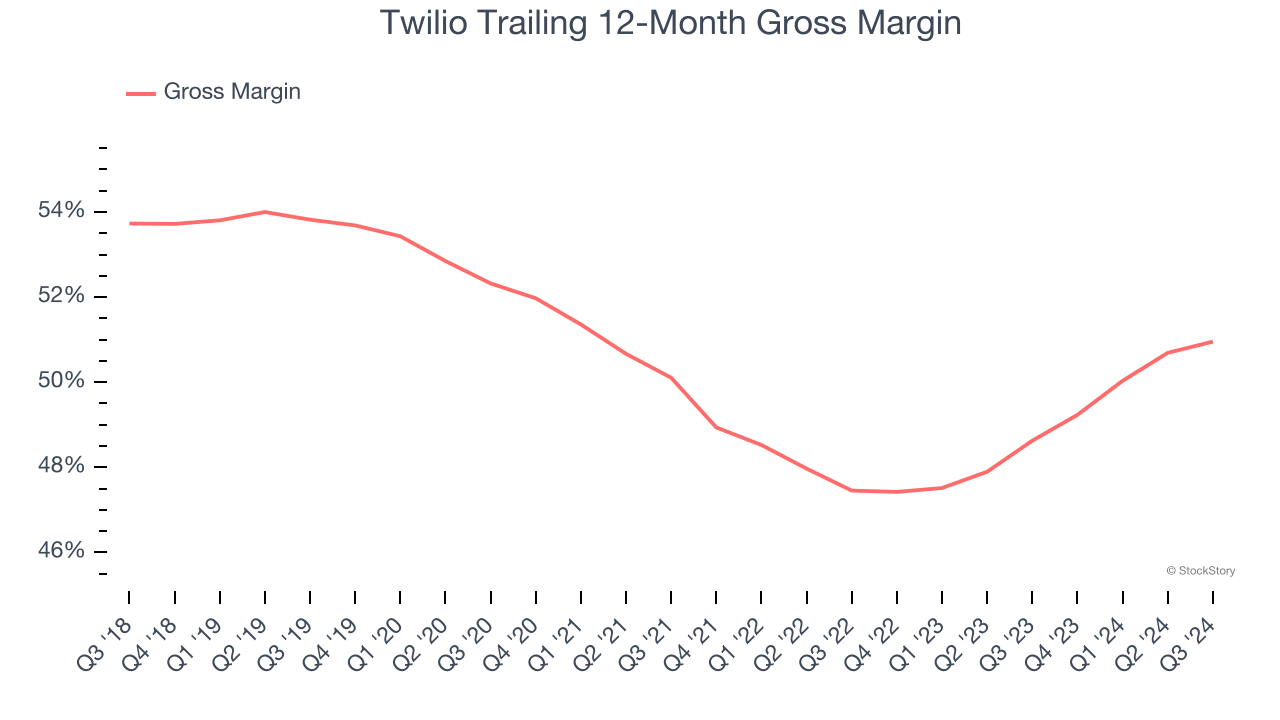

2. Low Gross Margin Reveals Weak Structural Profitability

For software companies like Twilio, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Twilio’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 51% gross margin over the last year. That means Twilio paid its providers a lot of money ($49.05 for every $100 in revenue) to run its business.

3. Cash Flow Margin Set to Decline

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

Over the next year, analysts predict Twilio’s cash conversion will fall. Their consensus estimates imply its free cash flow margin of 17.9% for the last 12 months will decrease to 14.6%.

Final Judgment

Twilio’s business quality ultimately falls short of our standards. Following the recent surge, the stock trades at 3.8× forward price-to-sales (or $111.06 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d suggest looking at KLA Corporation, a picks and shovels play for semiconductor manufacturing.

Stocks We Like More Than Twilio

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.