Smith & Wesson’s stock price has taken a beating over the past six months, shedding 28.3% of its value and falling to $10.04 per share. This was partly due to its softer quarterly results and might have investors contemplating their next move.

Is now the time to buy Smith & Wesson, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.Even though the stock has become cheaper, we're sitting this one out for now. Here are three reasons why you should be careful with SWBI and a stock we'd rather own.

Why Is Smith & Wesson Not Exciting?

With a history dating back to 1852, Smith & Wesson (NASDAQ: SWBI) is a firearms manufacturer known for its handguns and rifles.

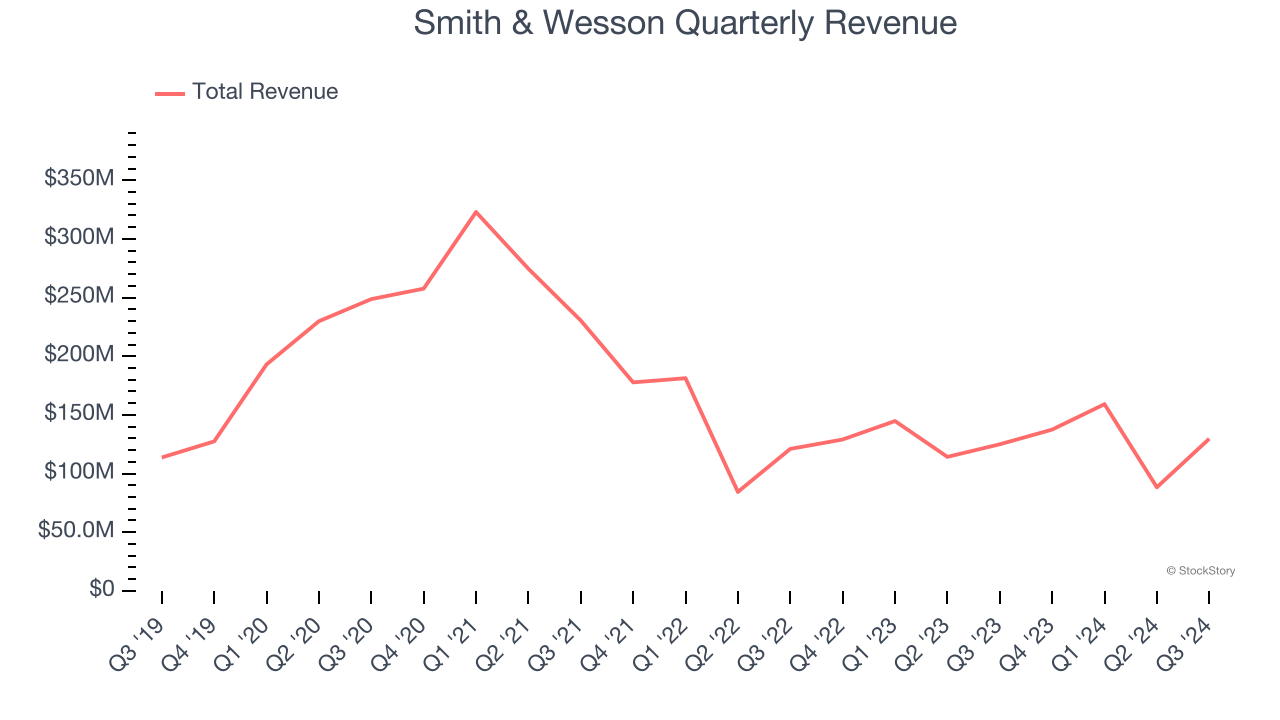

1. Revenue Spiraling Downwards

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Smith & Wesson’s demand was weak over the last five years as its sales fell at a 1.2% annual rate. This fell short of our benchmarks and signals it’s a lower quality business.

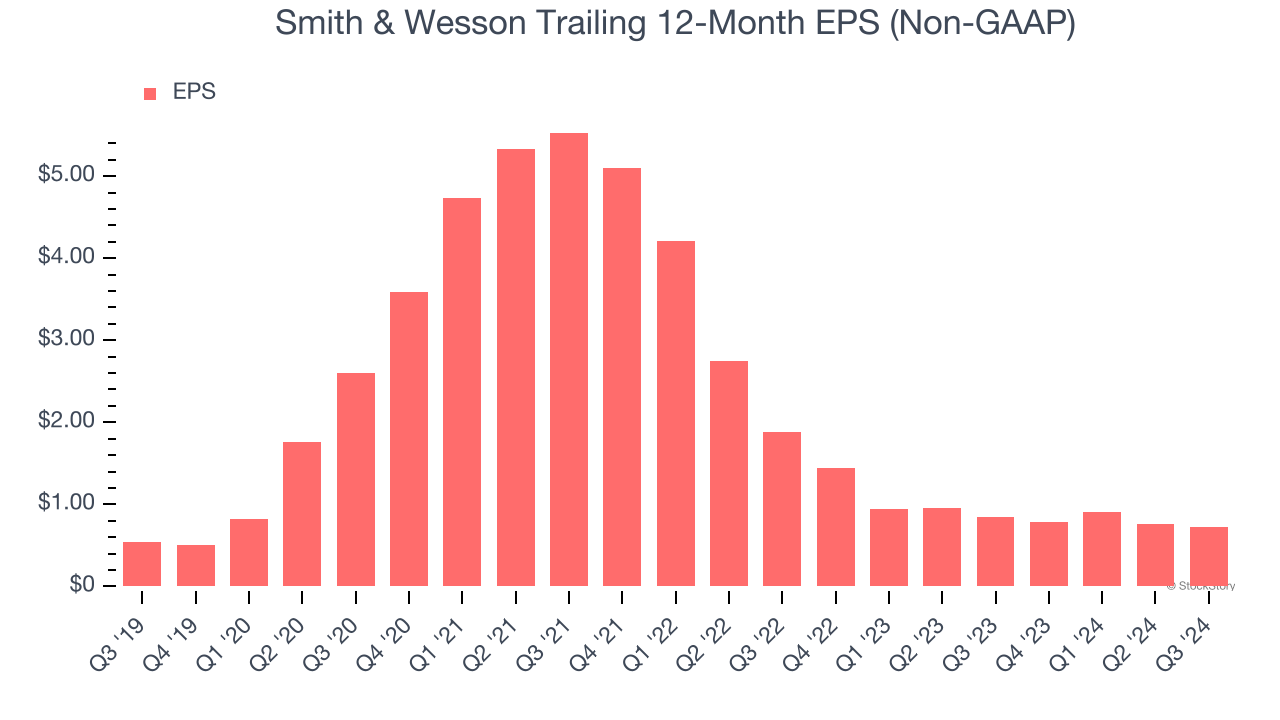

2. EPS Barely Growing

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Smith & Wesson’s EPS grew at an unimpressive 6.2% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 1.2% annualized revenue declines and tells us management adapted its cost structure in response to a challenging demand environment.

3. New Investments Fail to Bear Fruit as ROIC Declines

ROIC, or return on invested capital, is a metric showing how much operating profit a company generates relative to the money it has raised (debt and equity).

We typically prefer to invest in companies with high returns because it means they have viable business models, but the trend in a company’s ROIC is often what surprises the market and moves the stock price. Over the last few years, Smith & Wesson’s ROIC has decreased significantly. We like what management has done in the past, but its declining returns are perhaps a symptom of fewer profitable growth opportunities.

Final Judgment

Smith & Wesson’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 8.7× forward price-to-earnings (or $10.04 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're fairly confident there are better investments elsewhere. We’d suggest looking at ServiceNow, one of our all-time favorite software stocks with a durable competitive moat.

Stocks We Like More Than Smith & Wesson

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.