Over the last six months, Microsoft’s shares have sunk to $423.82, producing a disappointing 9.1% loss - a stark contrast to the S&P 500’s 6.3% gain. This might have investors contemplating their next move.

Given the weaker price action, is this a buying opportunity for MSFT? Find out in our full research report, it’s free.

Why Are We Positive On Microsoft?

Short for microcomputer software, Microsoft (NASDAQ: MSFT) is the largest software vendor in the world with its Windows operating system, Office suite, and cloud computing services.

1. Skyrocketing Revenue Shows Strong Momentum

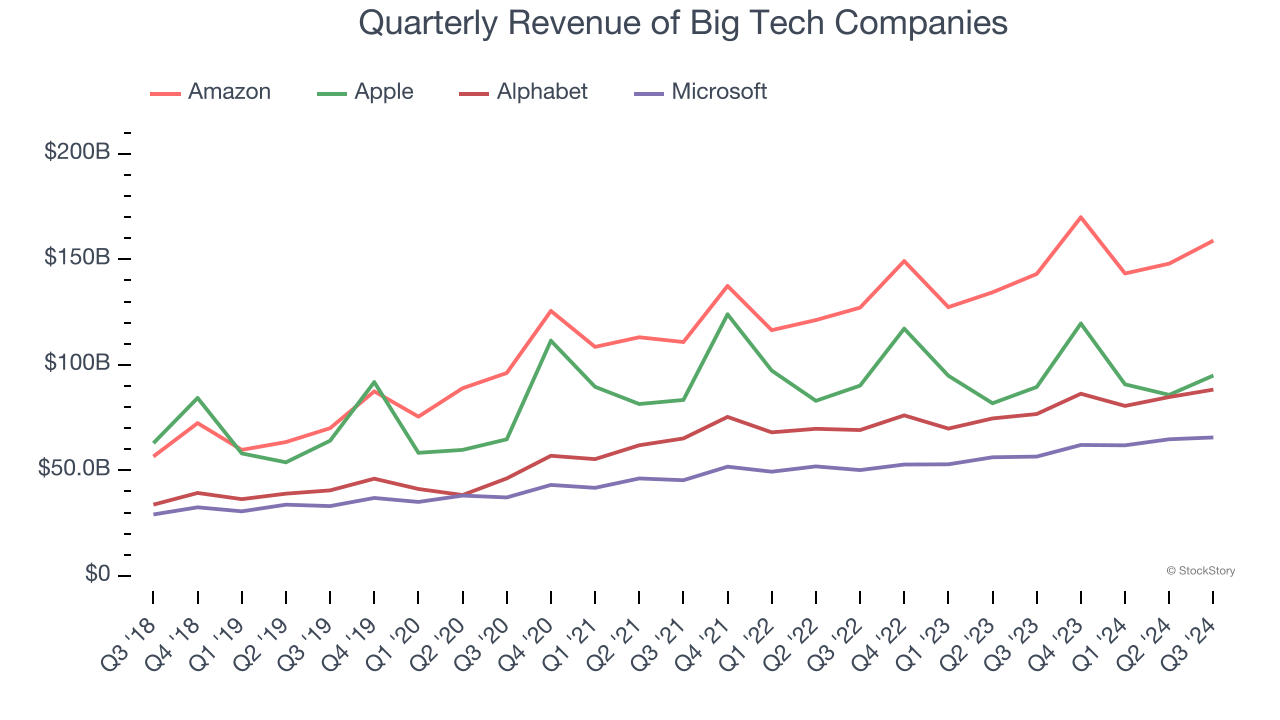

Microsoft shows that fast growth and massive scale can coexist despite the conventional wisdom about the law of large numbers. The company’s revenue base of $129.8 billion five years ago has nearly doubled to $254.2 billion in the last year, translating into an exceptional 14.4% annualized growth rate.

Over the same period, Microsoft’s big tech peers Amazon, Alphabet, and Apple put up annualized growth rates of 18.5%, 17%, and 8.5%, respectively.

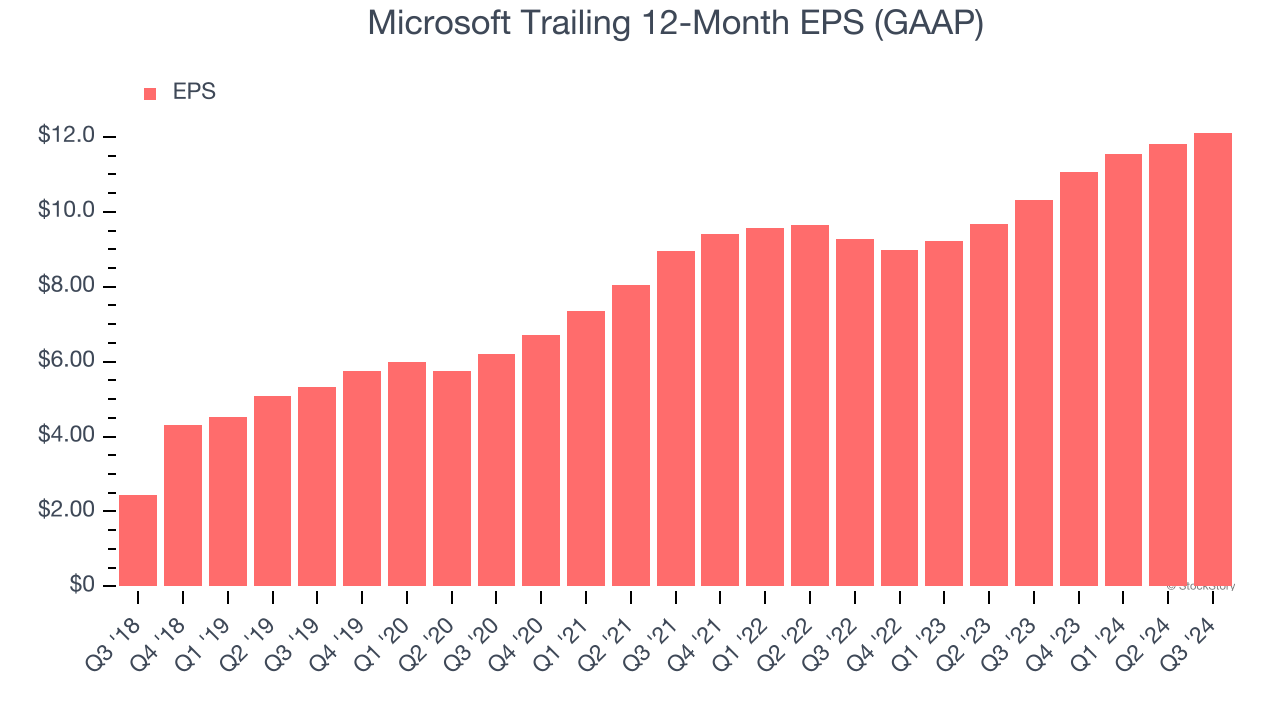

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it shows whether a company’s growth is profitable. It also explains how taxes and interest expenses affect the bottom line.

Microsoft’s EPS grew at an astounding 17.9% compounded annual growth rate over the last five years, higher than its 14.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

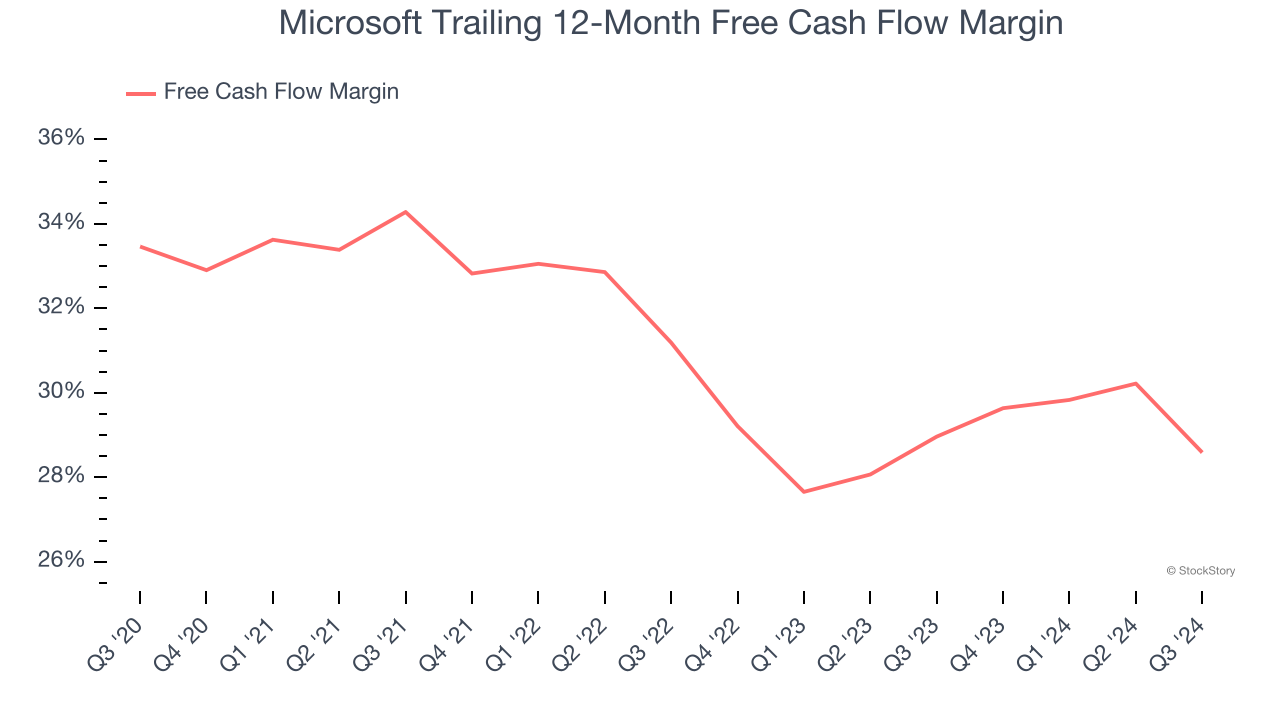

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills or invest for the future.

Microsoft has shown terrific cash profitability, driven by its lucrative business model that enables it to reinvest, return capital to investors, and stay ahead of the competition while maintaining an ample cushion. The company’s free cash flow margin was among the best in the software sector, averaging an eye-popping 30.9% over the last five years.

Final Judgment

These are just a few reasons Microsoft is a high-quality business worth owning. With the recent decline, the stock trades at 31.2× forward price-to-earnings (or $423.82 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free.

Stocks We Like Even More Than Microsoft

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like United Rentals (+550% five-year return). Find your next big winner with StockStory today for free.