What a fantastic six months it’s been for Limbach. Shares of the company have skyrocketed 51%, hitting $97.01. This was partly thanks to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is now the time to buy Limbach, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

We’re happy investors have made money, but we're cautious about Limbach. Here are three reasons why we avoid LMB and a stock we'd rather own.

Why Is Limbach Not Exciting?

Established in 1901, Limbach (NASDAQ: LMB) provides integrated building systems solutions, including mechanical, electrical, and plumbing services.

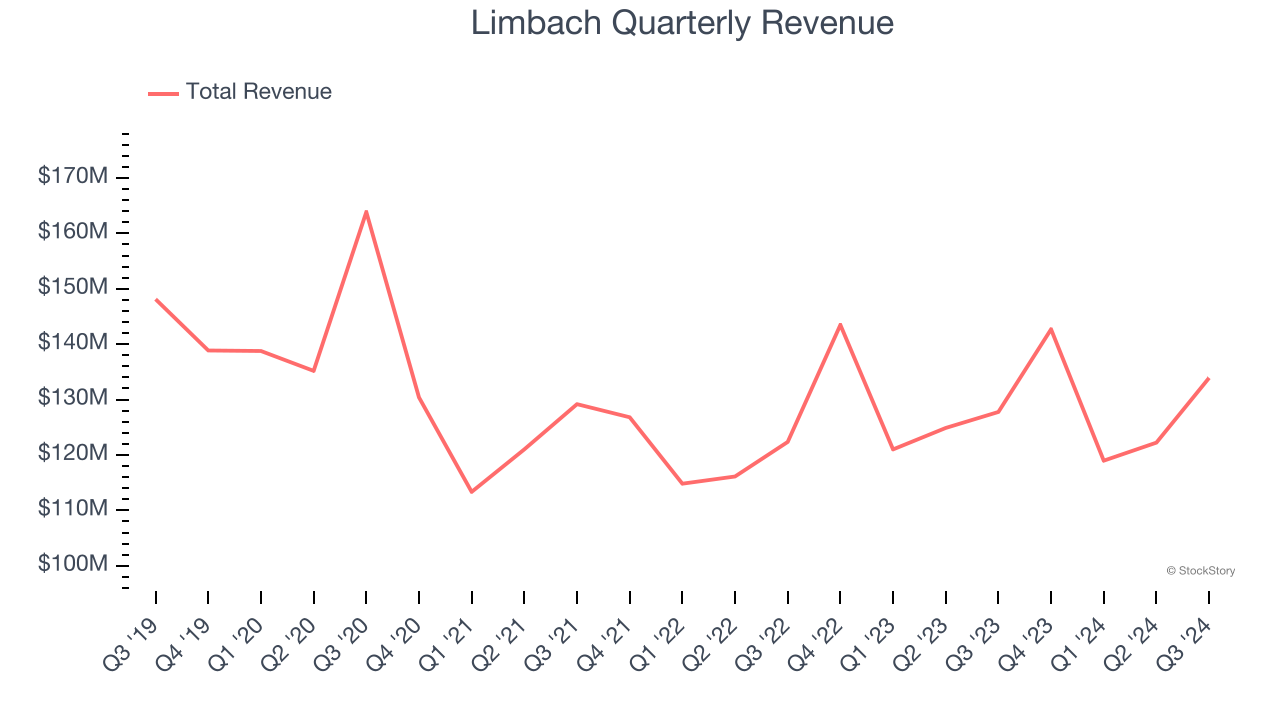

1. Revenue Spiraling Downwards

A company’s long-term performance is an indicator of its overall quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for years. Limbach struggled to consistently generate demand over the last five years as its sales dropped at a 1.8% annual rate. This was below our standards and signals it’s a lower quality business.

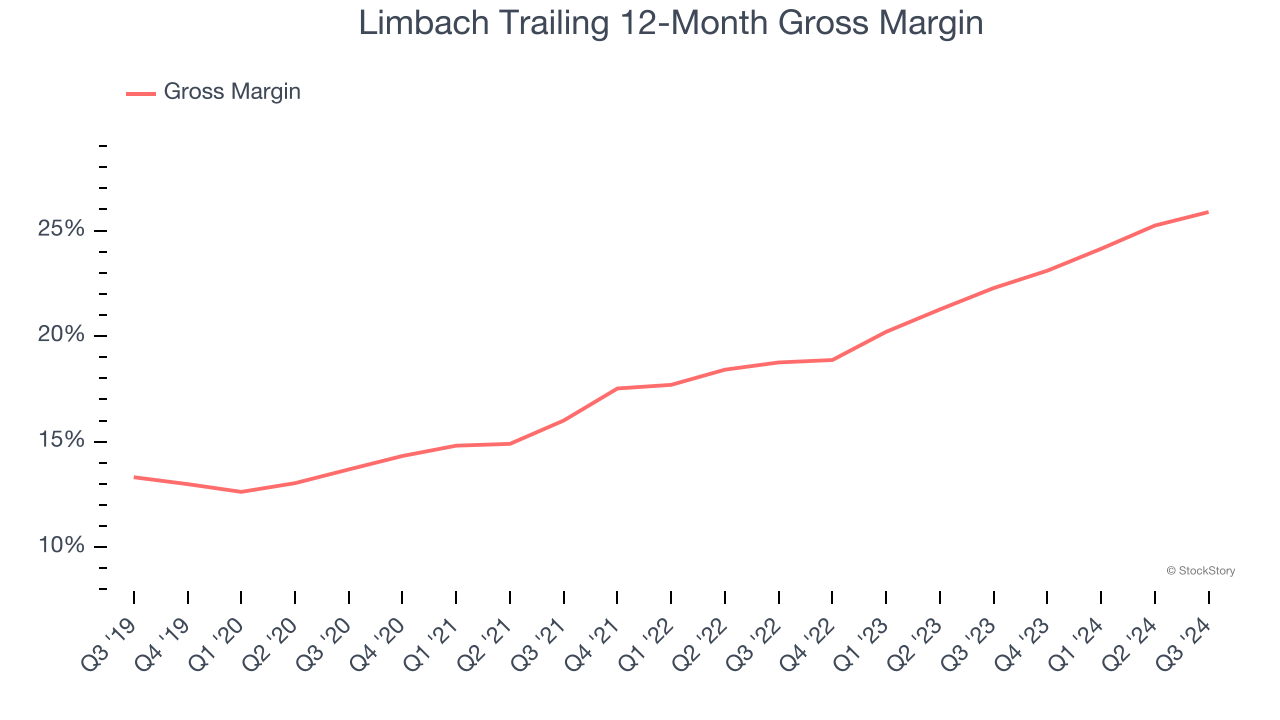

2. Low Gross Margin Reveals Weak Structural Profitability

For industrials businesses, cost of sales is usually comprised of the direct labor, raw materials, and supplies needed to offer a product or service. These costs can be impacted by inflation and supply chain dynamics in the short term and a company’s purchasing power and scale over the long term.

Limbach has bad unit economics for an industrials business, signaling it operates in a competitive market. As you can see below, it averaged a 19.2% gross margin over the last five years. Said differently, Limbach had to pay a chunky $80.77 to its suppliers for every $100 in revenue.

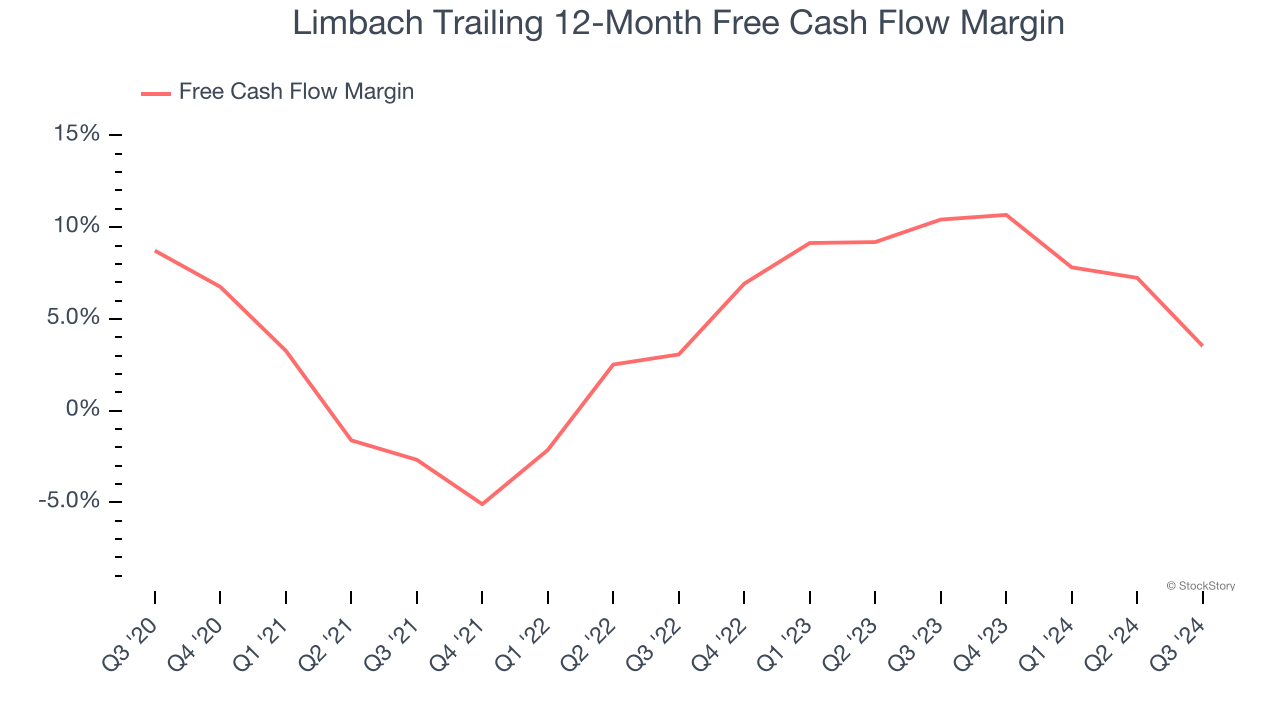

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Limbach’s margin dropped by 5.2 percentage points over the last five years. This along with its unexciting margin put the company in a tough spot, and shareholders are likely hoping it can reverse course. If the trend continues, it could signal it’s becoming a more capital-intensive business. Limbach’s free cash flow margin for the trailing 12 months was 3.5%.

Final Judgment

Limbach isn’t a terrible business, but it doesn’t pass our quality test. After the recent surge, the stock trades at 41.7× forward price-to-earnings (or $97.01 per share). This multiple tells us a lot of good news is priced in - you can find better investment opportunities elsewhere. We’d suggest looking at KLA Corporation, a picks and shovels play for semiconductor manufacturing.

Stocks We Like More Than Limbach

The elections are now behind us. With rates dropping and inflation cooling, many analysts expect a breakout market to cap off the year - and we’re zeroing in on the stocks that could benefit immensely.

Take advantage of the rebound by checking out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.