Snap-on’s 30.1% return over the past six months has outpaced the S&P 500 by 20.5%, and its stock price has climbed to $347.99 per share. This was partly due to its solid quarterly results, and the performance may have investors wondering how to approach the situation.

Is there a buying opportunity in Snap-on, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free.Despite the momentum, we're sitting this one out for now. Here are three reasons why there are better opportunities than SNA and a stock we'd rather own.

Why Is Snap-on Not Exciting?

Founded in 1920, Snap-on (NYSE: SNA) is a global provider of tools, equipment, and diagnostics for various industries such as vehicle repair, aerospace, and the military.

1. Long-Term Revenue Growth Disappoints

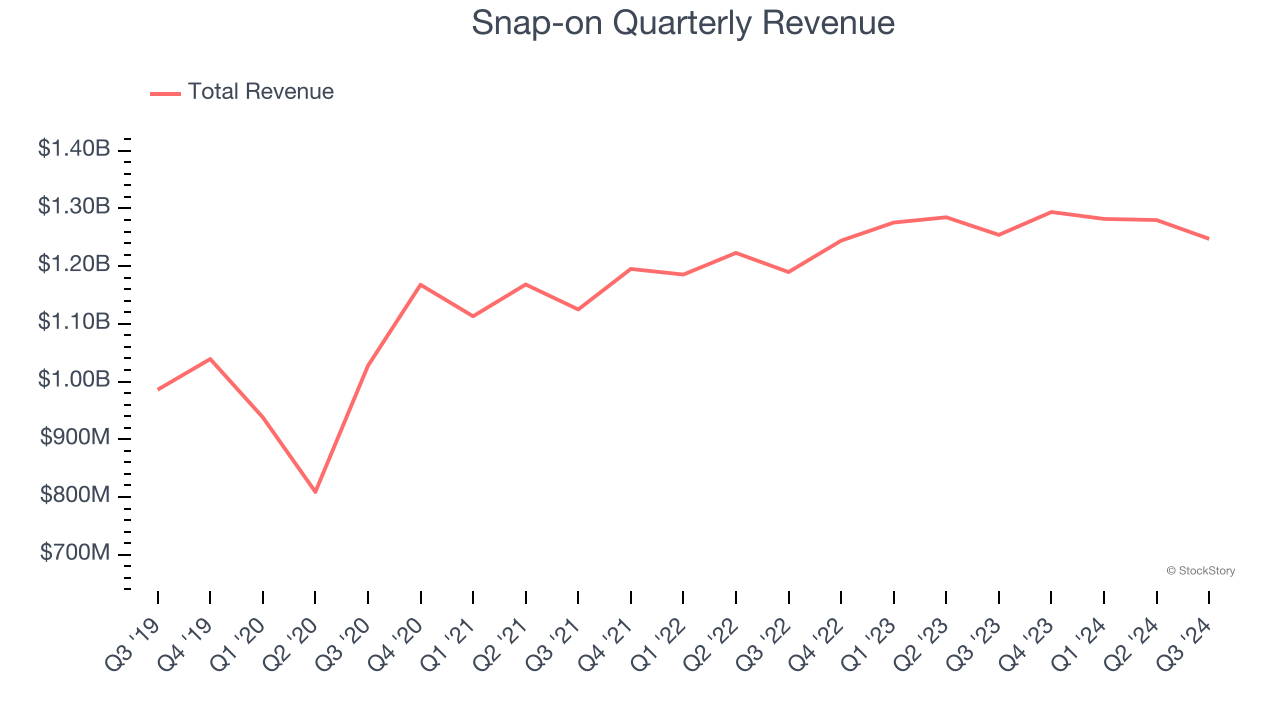

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Snap-on grew its sales at a tepid 4.7% compounded annual growth rate. This was below our standard for the industrials sector.

2. Core Business Falling Behind as Demand Plateaus

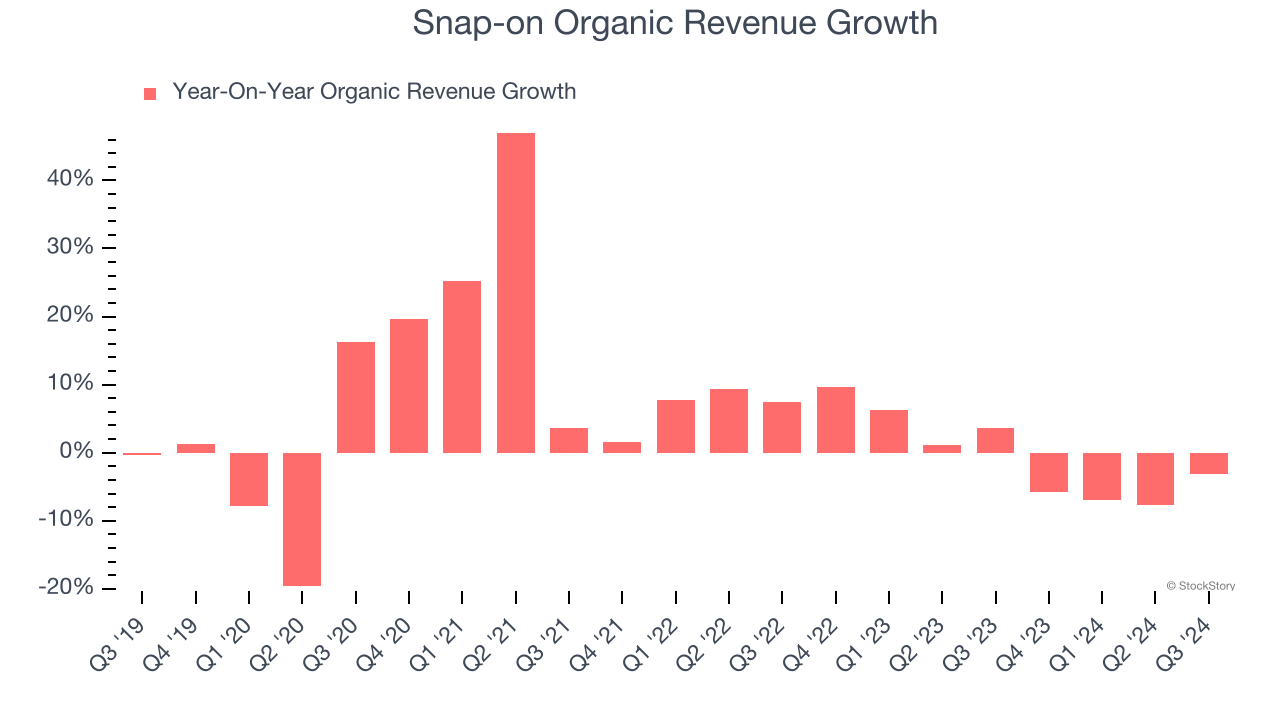

Investors interested in Professional Tools and Equipment companies should track organic revenue in addition to reported revenue. This metric gives visibility into Snap-on’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Snap-on failed to grow its organic revenue. This performance was underwhelming and implies it may need to improve its products, pricing, or go-to-market strategy. It also suggests Snap-on might have to lean into acquisitions to accelerate growth, which isn’t ideal because M&A can be expensive and risky (integrations often disrupt focus).

3. Free Cash Flow Margin Dropping

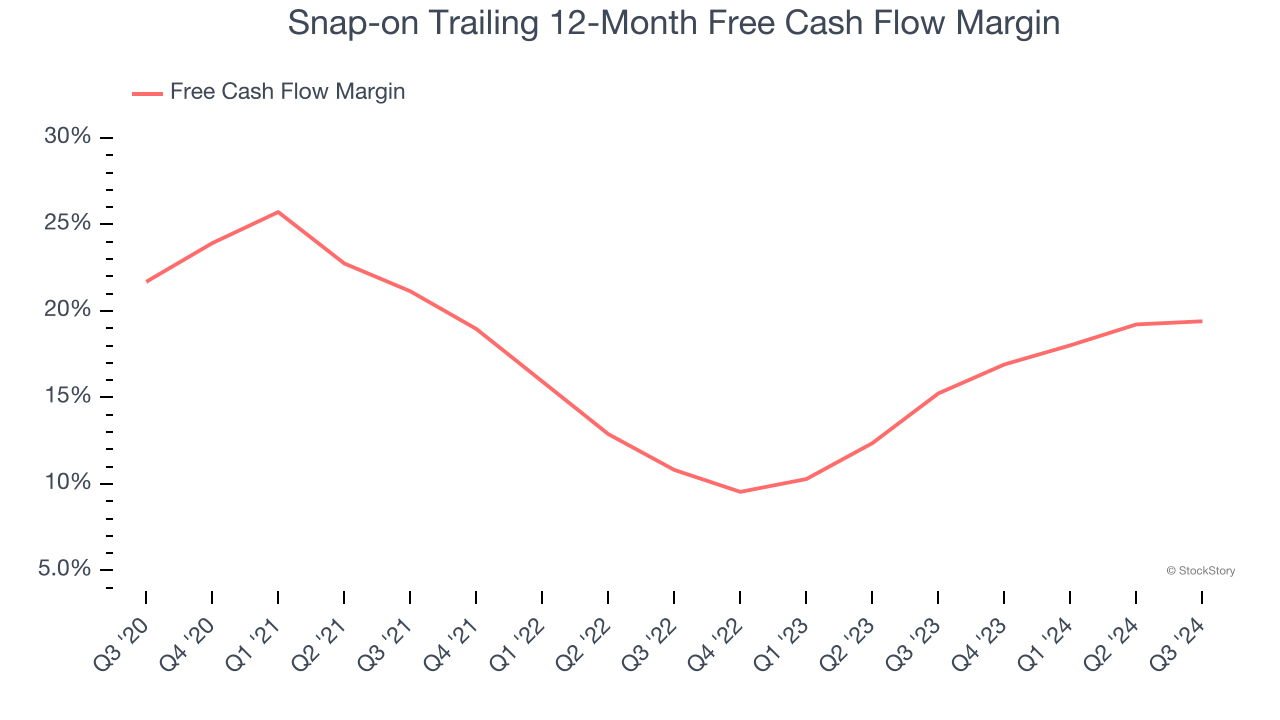

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Snap-on’s margin dropped by 2.3 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal higher capital intensity. Snap-on’s free cash flow margin for the trailing 12 months was 19.4%.

Final Judgment

Snap-on isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 17.5× forward price-to-earnings (or $347.99 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're fairly confident there are better investments elsewhere. Let us point you toward Google, whose cloud computing and YouTube divisions are firing on all cylinders.

Stocks We Would Buy Instead of Snap-on

The Trump trade may have passed, but rates are still dropping and inflation is still cooling. Opportunities are ripe for those ready to act - and we’re here to help you pick them.

Get started by checking out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,691% between September 2019 and September 2024) as well as under-the-radar businesses like Comfort Systems (+783% five-year return). Find your next big winner with StockStory today for free.